“Runaway Inflation” Won’t Be Getting Very Far on Foot

The “wage-price spiral” was the distinctively destructive form that inflation took in the 20th century. It’s unlikely to make a comeback anytime soon.

Trade unionism — or its absence — profoundly shapes inflation. This fact first dawned on John Maynard Keynes and other leading economists in the 1920s, and it was taken for granted in much of the mainstream analysis of inflation at least through the 1980s. Some faint, residual awareness of the connection is still ambient in the discourse, but by the time COVID-era inflation arrived, understanding of the idea, both in the broad public and among experts, had become murky and confused.

In a labor market dominated by strong collective bargaining, the process of wage-setting differs from that of an atomistic labor market not just quantitatively — in the sense that unions give workers more leverage and help them capture a bigger share of the economy’s proceeds — but qualitatively.

In a nonunion context, individual workers can exert leverage over their employers — at best — via the threat (explicit or implicit) of quitting. When a worker quits, the employer incurs the cost of filling the resulting vacancy: the costs of search, training, and a period of dampened productivity in the interim. To avert a quit, a rational and informed employer may be willing to concede higher wages. But the amount conceded should, in principle, be no greater than the expected cost

of filling the vacancy.

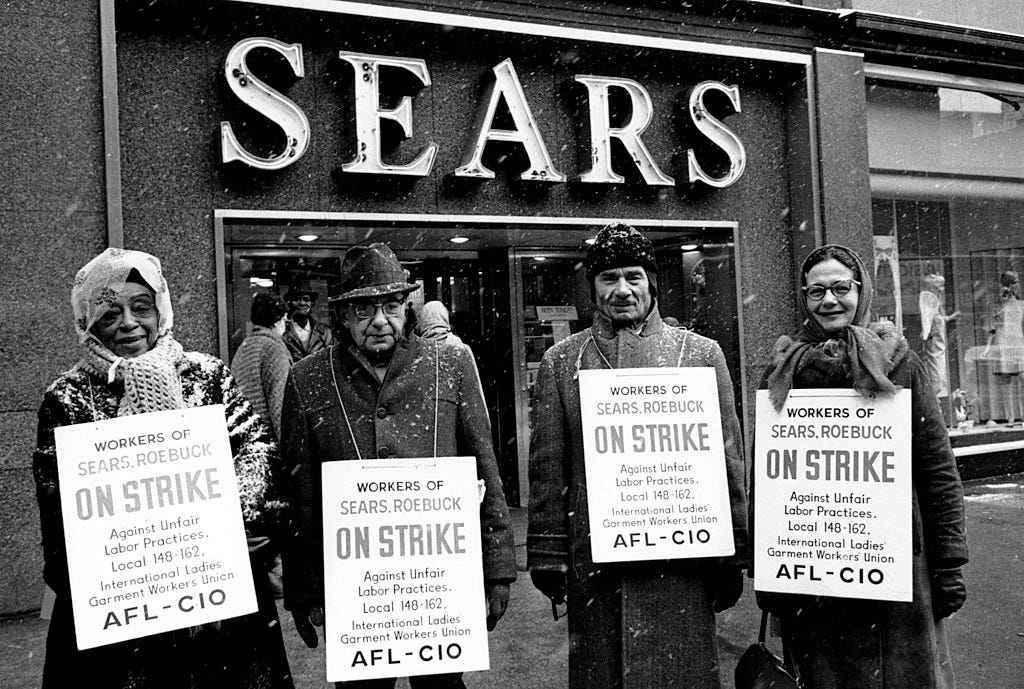

In a unionized context, workers exert leverage over employers not by threatening to quit, but by threatening to strike. A strike is like a quit in that labor is withdrawn from the firm in a way that imposes costs on the employer. But that’s where the similarity ends.

Unlike a quit, the aim of a strike is generally to shut down production entirely. And if successful, the cost it imposes on the firm amounts to the entire value of the firm’s output for the duration of the strike. Obviously, any firm that tries to get away with paying “too low” wages risks incurring a vastly greater penalty in a strongly unionized labor market than in an atomized one.

In fact, the penalty is so great, compared to the relatively paltry cost of vacancy-filling, that the real puzzle is why workers in a strongly unionized economy don’t capture an incomparably greater proportion of the output than they actually do, or than their counterparts in a nonunion economy do……