Productivity statistics, Paul Krugman, and Hicks's "shadows on the face of history"

Explaining why nonsensical numbers seemed to make sense.

In his Substack post mentioning my recent article, Paul Krugman makes a point that, as he says, is different from mine, but doesn’t contradict it: just because productivity grows faster in Country A than in Country B, that doesn’t mean Country A will necessarily get any richer relative to Country B.

This claim will surely strike many people as counterintuitive, if not incredible, which probably explains why Krugman takes the trouble to work through a detailed numerical example to demonstrate his point.

In Krugman’s example, the US tech sector experiences a productivity boom. But the boom leaves US GDP no higher relative to Europe — which lacks a tech sector of its own, in his stylized scenario — because with competitive markets, the increased productivity simply lowers US tech prices, which benefits Europe, too (or at least does it no harm.)

Krugman here is channeling the argument — or rather, half of the argument — made by John Hicks in his 1953 Oxford inaugural lecture, “The Long-Run Dollar Problem,” which, as it happens, was also about a US-Europe productivity gap.

What’s telling is that when Hicks made this argument — which today sounds surprising, if not heretical — he considered it to be nothing more than conventional wisdom. At the time, most English-speaking economists still lived in a mental world defined by the irenic liberalism of their Victorian forebears. If “classical economics,” as they called it then, had one big idea, it was that when one country (or individual, or class) progresses economically, everybody benefits; the economy isn’t a zero-sum game.

What prompted Hicks to revisit the question was the grim economic situation then prevailing in Europe, which seemed to discredit those comforting nostrums. Though we now remember the “postwar era” as a long, undifferentiated period of prosperity, that’s not how things looked in the late 1940s and early 1950s, when Europe was still struggling with intractable macroeconomic instability. The most visible manifestation of that instability, a malady we would now call a chronic balance-of-payments deficit, was then commonly referred to as Europe’s “dollar problem.”

The dollar problem seemed to pose an intellectual challenge to liberal economics because, in the judgment of most observers, its root cause was the enormous economic lead the United States had opened up vis-a-vis the Old World thanks to decades of breakneck productivity growth. Given how much more cheaply American firms could supply the market across a broad swath of industries, Europe appeared unable to sell enough exports to earn the dollars it needed to buy the very things (such as American machinery) it would need to catch up.

Some were now suggesting that Smith and Ricardo had been proven wrong after all. Maybe national economies could be harmed by other countries’ economic progress. Maybe the economy was, in some sense, a zero-sum game. In his lecture, Hicks set out to show that the tools of “classical” economics could both explain the dollar problem and define the exact conditions under which the old optimistic view would — and would not — hold.

The key distinction he drew was between what textbooks now call export-biased and import-biased growth. In the former, Country A’s productivity growth is beneficial to other countries because it’s concentrated in industries in which they do not compete. In the latter case, Country A’s progress can actually reduce the incomes of its trading partners, because it’s concentrated in sectors in which they formerly held a comparative advantage. Whether the irenic conclusions of classical theory hold or not is thus an empirical question that hinges on the actual pattern of trade and production:

I do think that we see the shadows of such patterns across the face of history. Western Europe is not the first metropolis of trade and industry which has suffered from the competition of the new lands which it has itself developed; there was, I fancy, an element of this same process in the decline of ancient Greece; we ourselves in this island grew great in the fifteenth century and later at the expense of the Flemish and Italian centres on which we had formerly depended. But though such historical examples warn us that the process under discussion is not at all uncommon, they also indicate that there is nothing inevitable about its denouement.

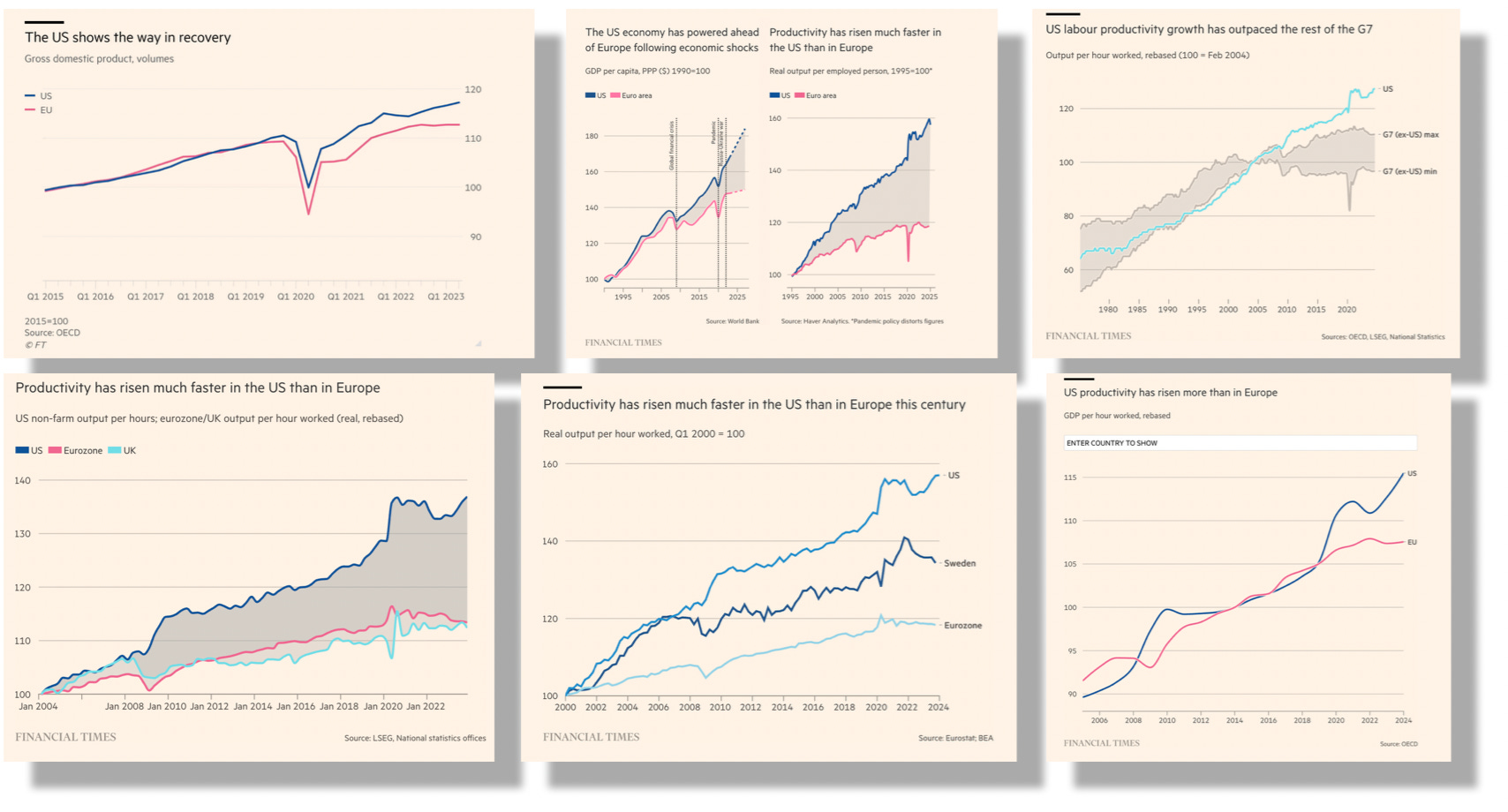

Since the 1980s, the default conventional wisdom has switched completely. You no longer have to convince educated people, as Hicks felt the need to do, that one country’s economic gain might be an another’s loss. “We live in a competitive world” is now the lowest common denominator cliché of economic discourse. This helps to explain why the business press has lately been full of charts like those below. The numbers just seem so perfectly in tune with the narrative: America’s world-beating tech industry is surging ahead. Surely Europe must be suffering the consequences.

(Sorry to pick on the Financial Times, which has been no worse than others.)

What I set out to show in my own article, on the statistics of US-Europe productivity comparisons, is that these numbers are almost certainly wrong.

The Hicks point is powerful. Productivity growth isn’t moral. It’s positional. If improvement happens in sectors where you don’t compete, everyone wins. If it lands directly in your comparative advantage, your income can fall even as global output rises. I see this in AI right now. Some firms are augmenting. Others are replacing. The difference determines whether the tide lifts you or drowns you. :)